The Birthright Fund

Make everyone a Bogle: buy 1% of the public markets every year, forever, and convey it to every birth certificate — a game designer's errata for the fertility attractor, with the lock, the ladder, and the keel that make it raid-proof.

Share this post:

Export:

Make Everyone a Bogle. Make America Fertile Again.

Three interactive models accompany this essay — a population-attractor calculator, a two-bloc world model, and the full Fund dashboard. Static previews stand in below while the live embeds finish their rollout; thirteen data plates are set throughout, captioned in place.

Prologue: The Kitchen

She's known for four days. The test is still in the bathroom drawer under the hair ties, because throwing it away makes it real in one direction and telling him makes it real in the other, and she hasn't decided. That's the word she keeps using in her own head. Deciding. As if it were a menu.

On the kitchen table: the folder. Daycare ran the numbers for her Tuesday — $1,840 a month, eighteen-month waitlist, and the woman on the phone was kind about it, which somehow made it worse. Under the daycare sheet, the student loans, $61,000 between them — his bootcamp, her master's. Under that, the mortgage they barely made in March. She has done this math nine times. It doesn't change. It isn't even close enough to argue with.

The garage door. At 4:40 in the afternoon. He is never home at 4:40. She decided an hour ago that tonight she tells him anyway — math or no math, people used to figure this out — and she has the sentence rehearsed, and she is standing up smiling when the door opens and she sees his face and the sentence dies in her mouth.

He sets his laptop bag on the counter. The badge is already off the lanyard; they deactivate those before the meeting ends now. Eleven years. He starts to explain it in the language it was explained to him, because he doesn't have his own words for it yet — the org is flattening, his team is being consolidated, they're "capturing synergies from our AI transformation across—" and he trails off. Last spring he wrote some of the documentation the thing was trained on. They both know it. There is no end to that sentence a man can say in his own kitchen.

The test stays in the drawer.

Nobody will ever count what happened in that kitchen. It will not appear in any statistic as an event, because the event is a thing that now won't happen — a child subtracted before arithmetic could give her a name. Multiply that kitchen by a few million a year and you have the number this essay is about: American women report wanting roughly half a child more than they have. Half a child, times everyone. That gap is the largest measured theft in the country, and no one was ever arrested for it, because the people who did the taking never entered the kitchen. They didn't have to. The bills on the table are their invoice.

I. The Attractor

Some catastrophes announce themselves: a siren, a date on a calendar. The one in that kitchen doesn't. It arrives one rational decision at a time, in full view, over decades — a strange attractor of economic and status incentives, gradient-descending toward collapse while everyone watches, because every actor's short-term reward function shadows the long-term pain function and defecting from the gradient is locally suicidal. Nobody jumps. Everybody slides.

The horror of this scenario is lucidity without agency. A civilization publishing papers about its own attractor basin, holding conferences on the slope it is descending, while every individual continues to surf. Worse, the visibility becomes part of the attractor's stability: once collapse is common knowledge, it gets priced in, discount rates on the future go vertical, and extraction accelerates. The attractor metabolizes awareness of itself into fuel.

This is not a thought experiment. One instance of it is running live, and it has been running for fifty years: fertility.

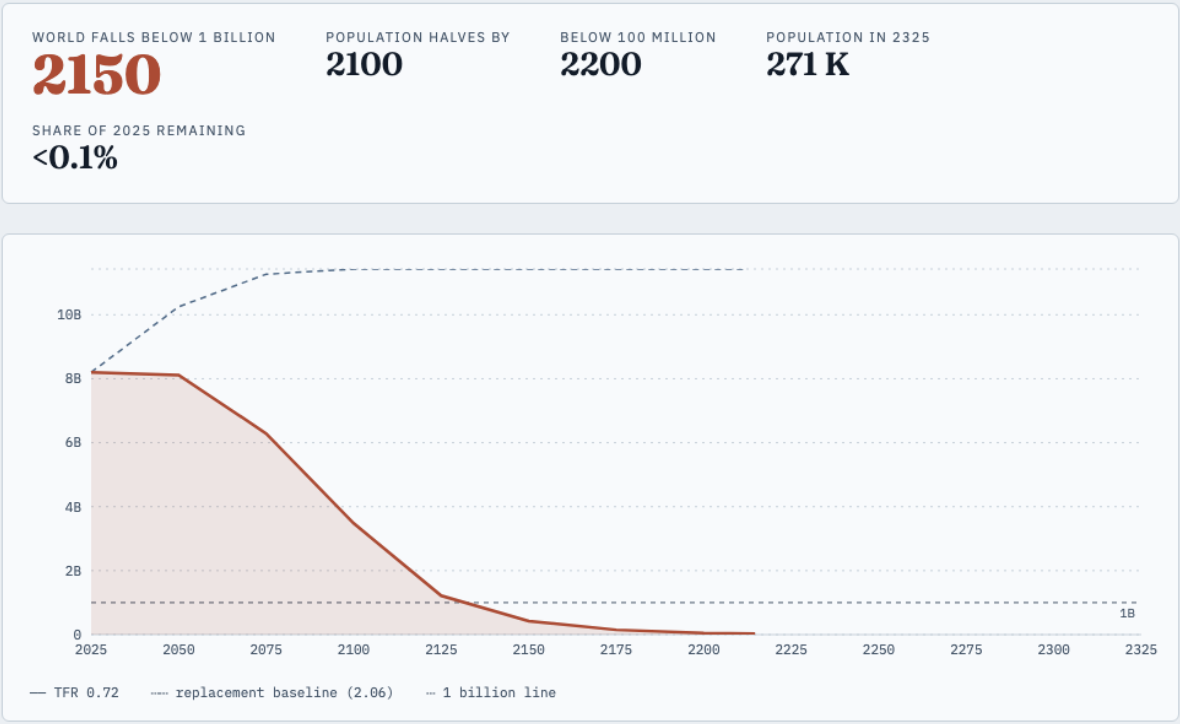

Global fertility has fallen from five children per woman in 1950 to 2.2 today. Seventy-one percent of humanity now lives in countries below the replacement rate of 2.1. South Korea sits at 0.72; Seoul at roughly 0.55. One number settles whether this is a cycle: no country that has fallen to very low fertility has ever returned to replacement. The attractor, so far, has no observed exits — only entries.

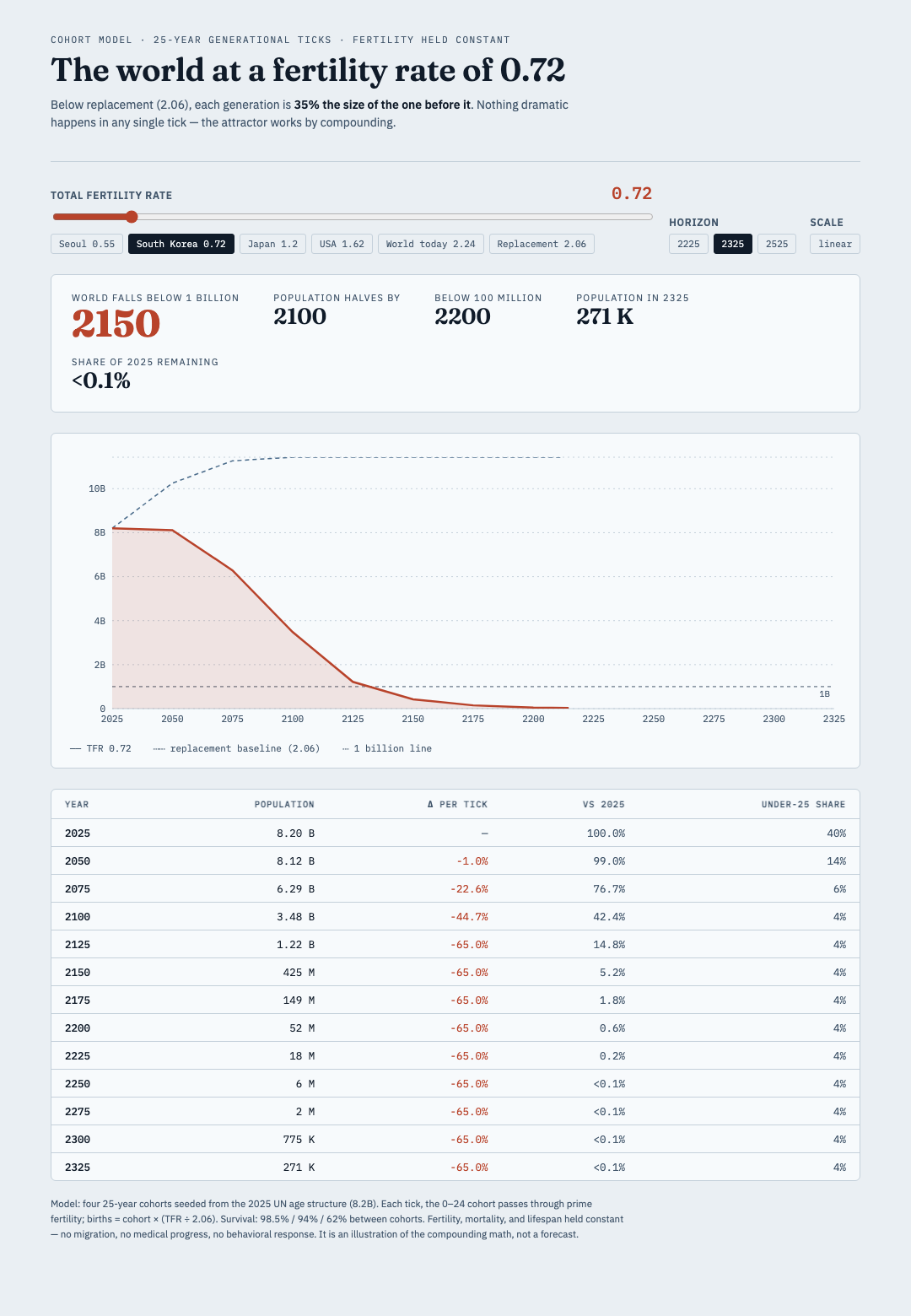

Run the arithmetic forward and it is not subtle. At South Korea's fertility rate, each generation is thirty-five percent the size of the one before it. The demographic curve looks gentle at first (a world locked at 0.72 drifts to seven billion by 2050 on momentum alone), but do not mistake the demography for the economy. Every institution of modern capitalism is a bet on growth: equity valuations are discounted claims on more customers, pensions are transfers from larger young cohorts to smaller old ones, sovereign debt is serviced by tomorrow's bigger tax base, and real estate is a call option on the next generation's demand. Walk into a venture meeting and say the quiet part out loud: fund my business — I promise 0.72 as many customers every twenty-five years. There is no financial system on Earth priced for that sentence. Mild demographic decline is severe economic contraction, and severe contraction is how fancy apes go back to smash and grab. The violence arrives decades before the emptiness does. Then the compounding takes over: below one billion in the mid-2100s, below one hundred million by 2200, single-digit millions by 2300. A planet built for eight billion, inhabited by a metro area. [Fig. 1 lets you run it yourself.]

The comforting objection is that the world is not South Korea — that above-replacement Africa breaks the pattern. It does not. Strip sub-Saharan Africa out of the global average and the remaining seven billion people are already below replacement at roughly 1.8. And Africa is not an exception to the basin; it is earlier on the same curve, moving faster. The fertility transition that took France a hundred and fifty years is taking Kenya about forty. Model the world as two blocs — a red below-replacement world and a blue above-replacement one — and under every historically grounded convergence assumption, the blue world overtakes the red on pure momentum around 2100, the global total peaks near nine billion, and then the whole structure tips into the same decline, with the demographic center of gravity relocated to Lagos rather than Shanghai. [Fig. 2.] Convergence does not change whether the attractor wins — only who is standing where when it does.

For twenty years the response to these curves has been think pieces. The seeing has changed approximately nothing. That is a bad empirical omen for lucidity as a strategy, and it is why this essay is not another diagnosis. I have spent thirty years designing games, so read what follows as a game designer's errata — material changes to make this game worth playing again. And I measure how fun an economy is by the most ruthless metric there is: how many babies are being born. Players who believe in the next round have children in it. Players who don't, don't.

II. The Graveyard Harmonic

To fix the attractor you have to find its engine. It has been running since Rome.

Historical demographers call it the urban graveyard effect: cities have never once in history reproduced themselves. Pre-modern London, Rome, and Edo ran death rates so far above birth rates that they could only maintain size — let alone grow — by continuously consuming rural population. E. A. Wrigley calculated that London circa 1700 needed thousands of net migrants a year merely to hold steady, absorbing a large share of England's entire natural increase. The magnitudes are debated at the edges; the direction is not. The city was always a demographic sink.

What modernity did was swap the mechanism while preserving the function. Disease was the old sink; opportunity cost is the new one. Seoul does not kill its residents anymore — it prices their reproduction out of existence. A total fertility rate of 0.55 is the graveyard effect running on real estate and credentialing instead of cholera.

Once you see the graveyard, the whole system resolves into a single multi-scale gradient, the same transfer function repeating at every octave. Village feeds town, town feeds regional city, city feeds capital megacity. Then the inter-country octave: Moldova feeds Poland, Poland feeds Germany, every node both predator and prey depending on which way you look. The countries with shrinking populations today are overwhelmingly middle-income — the six-to-twenty-six-thousand-dollar band that has lost its fertility but lacks the wealth to import replacements, sitting adjacent to richer economies that actively drain it. Eastern Europe is not uniquely infertile. It is donor tissue. The rich world's demographic stability is currently an extraction from the middle-income world — the same fractal gradient that empties villages into cities, running at planetary scale.

And the whole trophic column, from the village feeding the provincial town to sub-Saharan Africa feeding the OECD, has always been powered by one energy source: high-fertility peripheries. The system is a Ponzi of people, and over the last seventy years the extraction frontier ran out of planet. Rural Korea is empty. Rural China is emptying. Eastern Europe is exhausted. The base of the pyramid has stopped recruiting; the blue bloc is the last hinterland, and it is converging.

Here is the cruelest property of the gradient: it concentrates human beings precisely where reproducing them is most expensive. It is an anti-optimizer for fertility — the better it allocates labor to productivity, the better it allocates wombs to price floors. And the one clean counterexample on Earth tells you where the fix has to aim. Israel: fertility of 2.8 at high density and high income. Haredi Jerusalem and secular Tel Aviv sit on the same land prices. Density and wealth are not sufficient to collapse fertility. The gradient is economic; the sink is cultural — specifically, it is what happens when the child becomes a pure cost center whose lifetime returns accrue entirely to institutions rather than to the household that bore the cost. Fertility collapse is a rational producers' strike.

You cannot subsidize your way out of a strike. You can only change who owns the returns.

III. The Luckiest Coincidence

Now hold two facts side by side. The first is everything above: the world is running out of workers, on a schedule you can read off an age pyramid. The second is that we have just built a technology that manufactures workers.

I run a company in this technology, so let me report from the field rather than the op-ed page. On an ordinary day this month I ran six coding agents in parallel and happily paid five hundred dollars in API overages, because it was ROI-positive against hiring — one person operating what was recently a team's capital stock. And the morning I finished this draft, the AI news desk I run at BedrockNews landed the same pattern from the other direction: AI will hollow out the middle of every profession — the edges stay human. Six industries, one shape — the admin and routine-cognitive middle goes, the physical and high-judgment edges hold. The man in the kitchen is that middle. The pessimist reads "AI replaces labor" and "labor is disappearing" as two disasters. They are the same sentence with the valence flipped. The catastrophic version of the demographic attractor was always the dependency ratio — four retirees per worker, civilization as an understaffed hospice. The agents are the staff. The timing of AI's arrival, a decade or two before the rich world's pyramids fully invert, may retrospectively be the single luckiest coincidence in human history.

But only if the ownership question resolves correctly — because the same technology, differently owned, is the extraction gradient's final form. Intelligence is diffusing into every corporation as an input, like electricity. The productivity surplus will not accrue to "the AI companies"; it will condense wherever margins live — the insurer that cut claims costs, the lights-out warehouse, the tractor. Which means every scheme to share the gains by taxing a legally defined "AI sector" is a capture surface that the gains will simply migrate out of. Two examples make it concrete, because right now the hearings and the op-eds carry exactly one mainline thread, and it is "tax the AI." Suppose the robot tax passes: John Deere's autonomous tractor owes it, so Deere stops selling tractors and sells crop outcomes as a service — same machine, same margin, no robot on the invoice. Suppose the AI-profits levy passes: the frontier lab licenses its model at cost to the insurers and logistics firms that deploy it, the taxable "AI profit" rounds to zero, and the surplus reappears as a claims-processing margin in Hartford and a warehouse margin in Memphis, untouched. The gains are water; sector definitions are fences. Only the index is a bowl.

There is exactly one incidence-proof claim on a surplus whose location you cannot forecast: own the whole index. Wherever the value condenses, the index already holds it.

And the claim must be a stock, not a flow. Every income-transfer scheme — UBI in all its flavors — is an allowance: politically contingent, re-fought every budget, structurally a supplication. Ownership compounds, votes, and — the part that matters — constitutionally sticks. Alaska's Permanent Fund has survived every legislature since 1976 not because Alaskans are generous but because clawing an owned dividend back from every voter is political suicide, while trimming a welfare program is Tuesday. UBI is a policy. Universal ownership is a constituency. Only one of those defends itself.

History says the deal is purchasable. Table-flip deterrence has a strong record: Bismarck built the welfare state explicitly to defang the socialists; Britain extended the franchise in 1832 and 1867 with revolution visibly on the menu; the New Deal was sold to capital as cheap insurance against the alternative — and Huey Long's Share Our Wealth movement, a genuine American proto-authoritarian mass following, evaporated into Social Security offices. Elites share when the chits are credibly stompable and a mechanism is sitting on the shelf when the crisis makes it purchasable. The threat will supply itself. This essay is the mechanism.

And if you doubt the threat is already visible from the top, consider what the top is building. I personally know men worth eight and nine figures who are constructing bunkers — who tell me to my face that they see no path except widespread unrest, and who are stocking deep freezers with A5 wagyu and rosters of chosen staff. Douglas Rushkoff reported being paid to advise a room of such men whose most urgent question was how to keep their security guards loyal after money stops working; shock collars were floated, in apparent seriousness. These are men whose entire position is a stack of ownership claims — deeds, shares, account balances — preparing for the precise scenario in which ownership claims stop being honored, and their best answer to the contradiction is ribeyes and coercion hardware. They cannot turn a screw. Their claims survive exactly as long as the consensus pool that honors claims survives, and in the world they are provisioning for, they are not the lords of the compound. They are its best-marbled inventory. The bunker is a confession, the null hypothesis of the American elite poured in concrete: we expect the table to flip, and we intend to hide under it. This essay is addressed to the ones smart enough to prefer the other option, which has the additional advantage of having worked every time it has been tried: share the surplus, keep the civilization — and remain something other than meat.

IV. The Fund

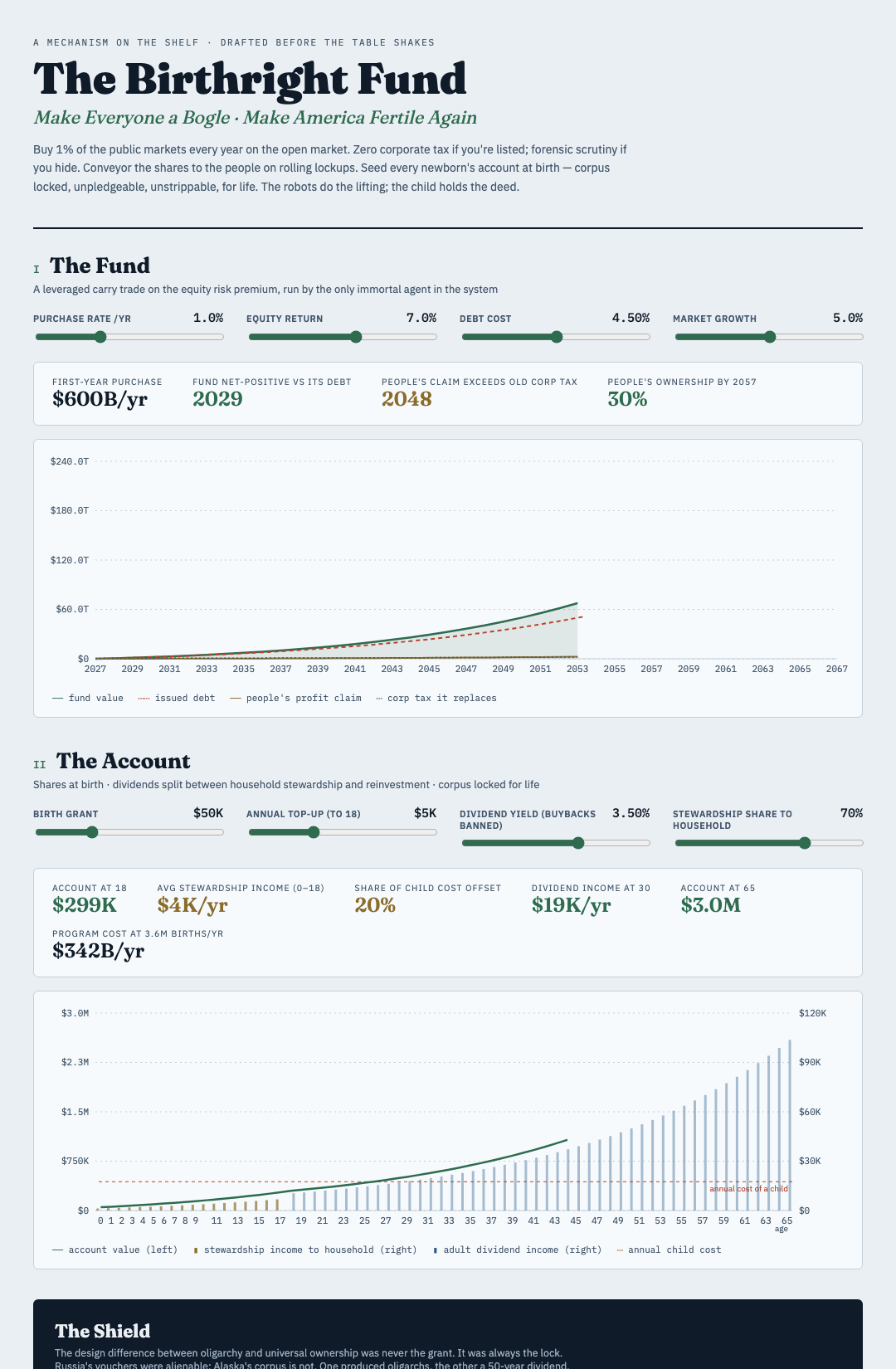

The mechanism is simple enough to fit on a chit: the United States purchases one percent of the public equity markets every year, on the open market, with issued debt, forever — and conveys the shares to the people.

One percent of a sixty-trillion-dollar market is about six hundred billion a year — roughly half of what America already spends annually on the Department of War and its Homeland Security paramilitary combined, and a rounding error against daily equity volume. The financing is a leveraged carry trade on the equity risk premium: issue debt near four and a half percent, hold assets returning near seven over long horizons. The equity premium is arguably the largest persistent unclaimed surplus in economics, and the poor cannot harvest it because harvesting requires collateral, duration, and the capacity to never sell at the bottom. The state is the only immortal, infinitely collateralized agent in the system. James Meade saw this in the 1960s: let the immortal entity bear the risk and pass the yield to mortals.

Every component has a live existence proof. The Bank of Japan bought its way to roughly seven percent of the entire Japanese equity market with printed money; markets did not break, and the position sits on enormous gains. Norway's fund owns about one and a half percent of every listed company on Earth. And the closest precedent to the full design is Hong Kong in 1998: the government bought roughly fifteen billion dollars of its own market to break a speculative attack, profited, and then distributed the position to citizens as discounted Tracker Fund units. The mechanism, executed once, under fire, profitably. What has never been tried is running it perpetually and universally.

The crisis behavior is the part the objections get backwards. A crash makes a fixed-dollar perpetual buyer purchase the same six hundred billion at lower prices — an automatic counter-cyclical stabilizer that gets richer on volatility. The "Japan took thirty-four years to break even" objection describes someone who bought once at the 1989 top, not a dollar-cost averager with an infinite horizon, who prefers a bad opening decade.

But the deepest justification is not that the trade is good. It is that we are already running it — with the legs reversed. The American state currently holds a massive uncompensated short put on the equity market. Every crisis proves the strike exists: TARP, the 2020 corporate credit facilities in which the Federal Reserve literally bought corporate bond ETFs, the GSE conservatorships, too-big-to-fail as standing doctrine. When markets fall far enough, the public balance sheet absorbs the tail. That is an insurance policy written by the taxpayer and exercised roughly once a decade, with the premium collected by someone else, since the top decile of households owns about ninety percent of the equities the public insures. Privatized gains, socialized losses is the slogan; the precise statement is that the public sells catastrophe insurance on corporate America and hands the premium to the policyholders. The Birthright Fund converts the naked short put into a covered position. If the public must eat the left tail, it should own the right one. And the receipts already exist: AIG's government equity stake exited at a gain of some twenty-two billion; the Fannie and Freddie preferreds returned tens of billions; the 2020 facilities wound down profitably; Hong Kong made money and gave it to citizens. The state buys at the bottom because that is when it is forced to act, and it cannot be margin-called in its own currency. The Fund simply runs the profitable half of the bailout continuously and on purpose, with the gains routed to birth certificates instead of to the shareholders it rescued.

Go one layer deeper and the ownership claim precedes even the insurance argument. The corporation is not a natural object. Limited liability is a state-granted option — investors' downside capped at their equity, the overflow landing on society — and the public has never charged for writing it. The public is the silent junior partner in every corporate charter: it absorbs the tail, supplies the courts, the property registry, the defense umbrella, the educated workforce, and, per Mariana Mazzucato's ledger, the foundational research under nearly everything from the internet to mRNA. Every private fortune is levered on that public equity. The Fund is not the state entering the market. It is the grantor of limited liability finally collecting its carried interest.

One more foundation, for the coalition that will never accept "redistribution": these AI models are compressed civilization, trained on the accumulated writing, code, judgment, and taste of everyone who ever published or committed. The training corpus is a commons that was enclosed. Universal equity in the machine economy is a royalty on expropriated input — the Georgist move, applied to the cognitive commons. Call it the Data Dividend, paid as title.

And watch how much of the current war dissolves under that one change of title. Every fight over AI right now is, underneath, a fight about uncompensated taking. The county board meeting screaming no data center in my backyard is really asking: why do I host the water draw and the substation load while the surplus wires out of town to someone else's shareholders? The artist's fury — how did they get my paintings, my prose, my songs? — is a claim for a royalty that was never offered. The rate-payer subsidizing gigawatt campuses, the town watching its aquifer feed cooling towers, the writer finding her voice in a model's output: every one of these is the same grievance in different clothes, and every one is currently being answered with public relations instead of equity. Now re-run each scene with the Birthright Fund in place. The data center rises in your county and your children's accounts hold the company building it. The model trained on your writing pays you the way a mineral lease pays the rancher — not because a court finally parsed fair use, but because you own the extractor. The angst does not have to be argued away. It capitalizes. Opposition to the machine is almost perfectly proportional to exclusion from its cap table, and the cap table is the one thing this plan changes for everyone at once.

V. The Great Swap

Here is the exchange that turns the Fund from a program into a new settlement: if you are public, your corporate income tax is zero. If you are private and large, you face the strongest transfer-pricing and cross-border scrutiny the state can field.

The corporate income tax is the worst instrument in the code — when the OECD ranked the major taxes by damage to growth, it finished dead last — its incidence leaks unpredictably onto workers and consumers, it biases firms toward debt, and it burns real resources on avoidance. More important, it is an adversarial flow claim: twenty-one percent of whatever profit you fail to hide, which makes hiding the rational sport. The swap replaces it with an aligned stock claim. The people's fund wants reported profits maximized, and a company paying zero has no reason to hide them. The entire concealment industry — the Dublin sandwiches, the Cayman IP shells — exists solely because of rate differentials. For the covered set, that industry isn't defeated; its reason to exist is deleted. Reported profits become honest for the first time in a century because honesty stops costing anything.

The arithmetic of the swap: corporate tax raises roughly five hundred billion a year; the Fund's pro-rata claim on now-untaxed profits crosses that figure somewhere around year twenty and grows forever after. The transition gap is financed by the same debt issuance already in the mechanism, and partially self-offsets, because announcing zero corporate tax reprices the entire market upward — which is why sequencing matters enormously: buy first, then cut, so the public captures its own policy's windfall rather than gifting it to incumbent holders.

The geopolitics is Delaware at civilizational scale. A state of under a million people is the legal home of two-thirds of the Fortune 500 because America already runs "attract the registry" as a business model. Offer the world's multinationals zero — not Ireland's twelve and a half — in the deepest capital market on Earth, in exchange for listing where the people's fund shops, and the inversions run in reverse. The residual corporate tax becomes what it always should have been philosophically: not a tax on profit but a tax on non-participation in the commons. Privacy remains legal. It just stops being subsidized.

The plain cost is a treaty war: under the OECD's global minimum tax, other countries could claim the right to collect the top-up on untaxed American profits. The United States would have to establish that a mandatory universal-equity structure constitutes an equivalent levy — an ownership-in-kind tax, which is exactly what it is — or be willing to break the framework. Given that the swap makes America the registry of world capitalism, the leverage exists. But it is a war, and I put it in the ledger as one.

The Kitchen, Two: October

Three months. The severance lasted nine weeks, and COBRA took $1,940 out of every one of them. He has had four final-round interviews; two of the first-round screens were conducted by software, which he did not mention to her, and which she knew anyway. The question in the drawer answered itself in August, the way questions do when you wait long enough. Neither of them says so out loud.

What they say out loud is the mail. The bill from her night in the emergency room — $4,212 after insurance, a number that exists because the cash price was never offered. The loan servicer that has started calling his cell at dinner, a company that bought the right to his future for cents on the dollar and would like to discuss his options. The letter from the county: the assessment is up eleven percent, on a house they are nine days from being late on.

Everything on that table is legal. Every party that touched this family in October is up on the quarter.

This is what the middle of the machine looks like from underneath. The next three sections unbuild it: first the account and its lock, then the rules that make a family's floor something no one is permitted to farm.

VI. The Account and the Shield

Now the half of the design that answers the fertility strike: every child born receives, at birth, an account seeded with index units — and the account is armored in a way no universal endowment has ever been armored before.

The mechanics: a birth grant on the order of fifty to seventy-five thousand dollars in units, annual top-ups through age eighteen, dividends split between reinvestment and a stewardship flow paid to the household while the child is a minor. At plausible parameters the account crosses three hundred thousand dollars around age eighteen and compounds to seven figures by retirement, throwing off dividend income the whole way. At 3.6 million births a year, the seeding costs a few hundred billion — inside the purchase envelope the Fund is already running. [Fig. 3, Section II.]

But the grant is not the design. The lock is the design. History ran the controlled experiment. Russia, 1992: every citizen received privatization vouchers — universal, per-capita ownership of the national asset base, philosophically identical to a birthright fund. The vouchers were freely alienable. Within three years they had been aggregated by the sophisticated for kopecks on the ruble, and the result was not universal capitalism but the oligarchy — the most concentrated expropriation in modern history, executed through a universal grant. Alaska made its corpus untouchable and paid only the dividend, and fifty years later the claim remains universal. The Homestead Acts and the Dawes allotments tell the same story. Every alienable universal endowment in history has re-concentrated within a generation, and the mechanism of re-concentration is always credit against it. Desperation plus a pledgeable asset equals a stripping industry.

So the birthright shares are inalienable the way the vote is inalienable — franchise, not property. And the legal technology is not exotic; it is centuries old and battle-tested. The spendthrift trust. ERISA's anti-alienation rule, which is why no payday lender has ever repossessed a 401(k). The Social Security anti-assignment statute. The critical feature these share is subtler than criminalization: contracts against the protected asset are not merely illegal — they are void and unenforceable. If lending against the shares were only criminal, an offshore gray market would form and prey anyway. If the contract is void — if no court will ever help the lender collect, and the borrower can walk away owing nothing — then no rational capital extends the loan in the first place. The predatory market is not policed out of existence; it is never able to form. Unenforceability is a better wall than prison.

The full armor: corpus unsellable for life (the dividend is yours to spend; the principal is citizenship), no collateral pledges ever, bankruptcy-remote, immune from civil judgment and garnishment — including by the state itself, which is otherwise history's most efficient stripper — separate property in divorce, with child support as the one debated carve-out. And the same reclassification extends to the two debts that currently strip young households at scale: medical and student debt cannot attach to protected assets, and are re-classed as non-recourse. The predictable objection — lenders will flee — is the intended effect, because in both sectors the credit was never financing the price; it was inflating it. The New York Fed found roughly sixty cents of each subsidized student-loan dollar passing straight through into tuition. Hospitals' cash prices already run below insurer-negotiated rates for identical procedures. Kill the enforceability and both sectors reprice to what buyers can actually pay — exactly as the uninsurable corners of medicine, LASIK and cosmetic surgery, have seen real price declines for decades while insured medicine inflated. Phase it in over a decade so the repricing is a glide, not a cliff.

Wealth you cannot lose is a different kind of thing than wealth you happen to have. The difference is what makes it a floor — and the floor, not the cash flow, is the fertility mechanism. The design difference between oligarchy and universal ownership was never the grant. It was always the lock.

VII. The Ladder

Ownership without market structure decays into a prettier oligarchy, so the Fund travels with a constitution for the market itself. Its design goal is not economic elegance. It is capture-resistance: make it structurally hard to buy the Senate.

The rules, bottom to top. Below ten billion dollars in enterprise value: full private freedom — family firms, startups, partnerships, privacy intact. At ten billion: mandatory public listing. The deal is transparency and a growing citizen stake in exchange for zero corporate tax; opacity above this line is what senate-buying fortunes are made of, and the fortunes that have most effectively purchased American policy have been overwhelmingly private structures with no disclosure, no proxies, no shareholders to answer to. From ten billion to one trillion: open running room — a hundredfold growth runway inside the transparent pool. At one trillion, indexed to roughly three percent of GDP: automatic functional separation. And the clock is short, because the surprise is zero: a four-hundred-billion-dollar company can see the tripwire from years away, so the statute makes it look officially — at half the threshold, the firm files its separation plan; on crossing, it has eighteen months to execute, spinning constituent businesses into independent listed companies, shares distributed pro-rata to every holder, including every birthright account. An organization with the smartest people and deepest resources on Earth does not need five years to do what its own bankers would gleefully do in one. No discretion, no decade in court.

Alongside the thresholds, two flow rules. Buybacks are banned — a repeal of the SEC's 1982 safe harbor, restoring the pre-1982 treatment of repurchases as manipulation — because in a system where corpus is locked, buybacks route surplus into price gains trapped behind the lock, while dividends route it into stewardship income at kitchen tables. Redirect today's roughly trillion-dollar annual buyback flow into dividends and the market's yield rises from about 1.3 percent toward 3.5 or 4 — which alone triples the household income the birthright accounts generate. And acquisitions by firms above one hundred billion are barred: build it, license it, or lose to it. The killer-acquisition literature (Cunningham, Ederer, and Ma in pharma; Kamepalli, Rajan, and Zingales on the venture "kill zone") documents the disease; the cure re-routes the startup exit toward the IPO at the ten-billion door, feeding the commons instead of the incumbent's moat. The true cost — softer seed-stage pricing while the restored IPO channel replaces acquisition premiums — is a transition, not a wound, and the sharper long-term version of the rule is behavioral rather than size-based: bar acquisitions that discontinue the product.

The theoretical spine of the Ladder is Mancur Olson: small groups organize cheaply; capture is a coordination problem, and fission raises its cost. Three trillion-dollar firms with aligned interests can buy a senate over lunch; thirty three-hundred-billion-dollar firms with competing interests produce lobbying that partially cancels. Pair Olson with Gilens and Page's finding that American policy tracks organized-interest preferences while the median voter shows near-zero independent effect, and the Ladder reads as a direct mechanical answer to the best-documented pathology in American political science.

The reflex objection is national champions: that fission disarms America while Beijing consolidates. The history runs precisely backwards. Innovation's empirical record is that concentration funds research and strangles deployment, and fission releases the inventory. The 1956 AT&T consent decree forced Bell to license every patent royalty-free — including the transistor — and seeded the entire semiconductor industry; the 1984 breakup released what Bell Labs had warehoused. Fairchild fissioned out of Shockley, Intel out of Fairchild; Silicon Valley is itself a fission product. And the pattern is running again right now, in the industry I work in: Google invented the transformer, and all eight authors of the paper left — the frontier advanced exactly as fast as researchers could escape the balance sheet whose search-ad monopoly could not let them ship. Apple, with thirty billion a year of R&D and the greatest engineering organization ever assembled, cannot find first gear in AI, because Arrow's replacement effect is not a metaphor: the incumbent innovating merely replaces profits it already has. Meanwhile China's genuinely fearsome sectors — EVs, batteries, drones — were forged not by national fists but by hyper-Darwinian domestic competition among hundreds of entrants; where Beijing consolidated and disciplined its tech giants, the engine sputtered. Champions don't innovate. Escapees do. Our advantage over China has never been the size of our fists; it is that our system lets the fingers leave. The Ladder guarantees the frontier always has somewhere to escape to — and under the Fund, every escape pays a dividend to every child in the country.

As for capital intensity — the real steelman, since frontier training runs and fabs need tens of billions of coordinated capital — the current AI buildout is the existence proof against it: the frontier labs are financed not by retained monopoly earnings but by capital markets, which the Fund makes permanently deeper. Where genuine physical-scale exceptions exist, the answer is the regulated-utility toolkit, not exempting trillion-dollar generalists from the blade because one division pours concrete.

VIII. The Hearth and the Tithe

The mirror-image pair: the floor is never taxed; the peak is always taxed.

The Hearth. By constitutional amendment, no property tax on a primary home valued below twice the local median. The paid-off family home is currently rented from the county in perpetuity — stop paying the tax and discover who really owns it. Under this rule the hearth becomes true corpus, unstrippable like the birthright shares. And it is not symbolic for the fertility thesis: the strongest causal evidence in the entire fertility literature is a housing-wealth result. The revenue backfill is the Georgist move — land-value-weighted rates on investor-owned and non-primary residential property, which simultaneously replaces school funding and disarms the institutional-landlord bid that has been outcompeting young families for starter homes. Housing as shelter, untaxed; housing as extraction, taxed harder. The same asset, taxed by use, the way this whole system treats capital everywhere.

The Tithe. A two percent annual tax on personal wealth above fifty million dollars, realized or not, with an exit tax with teeth for expatriation. Every European wealth tax died on two blades: valuation of illiquid fortunes and flight. The Ladder already solved the first — mandatory listing at ten billion means the valuations Europe's tax authorities died guessing at print daily at four in the afternoon. Switzerland's century-old wealth tax, the one that survived, works precisely because valuation is mechanical; this design is the most mechanical valuation regime imaginable. Constitutionality — the apportionment problem for direct taxes — is answered by bundling authorization into the same amendment as the hearth exemption: the tax on peaks and the immunity of floors ratified as one bargain, so nobody votes for the mansion's protection without voting for the billionaire's tithe.

And notice the dynamic: paying two percent annually on equity requires selling roughly two percent of one's shares a year — into a market where the people's fund is the permanent bid. Concentrated wealth is not confiscated in this system; it is metered out into universal ownership at two percent a year, forever. The tithe is the pump; the Fund is the reservoir. Compounding still wins for the wealthy — seven percent returns minus a two percent tithe leaves real growth; sharks remain sharks. But the share of the machine held by whales versus citizens ratchets in one direction only.

The lock-in problem needs the same treatment from below. The current code maximally punishes selling — high capital-gains rates plus step-up basis at death, which together produce buy-borrow-die: never realize, ever. Trillions in shares are frozen not by conviction but by tax architecture, which is float the market needs for price discovery. The trade: lower the rate on long-held assets and abolish step-up at death — the carrot and the deadline together, unlocking a genuine standing sell flow from the mass-affluent tier to complement the tithe's flow from the whales. Buy-side pump, sell-side pump.

IX. The Keel

Institutions are consensus pools. The world is still, at bottom, run by clever apes throwing fast rocks, and no parchment stops a regime willing to ignore parchment. A constitution's real function — Hume's insight, Hardin's gloss — is coordination: it tells millions of apes when to throw rocks together and at whom. The amendment that protects the Fund is therefore designed not as a wall but as a tripwire wired to three hundred forty million alarms.

The raid record teaches the clauses. Hungary, 2011: a populist government coerced fourteen billion dollars of mandatory private pension assets back into the state in one legislative season. Poland, 2013: the bond half of the pension system nationalized with an accounting argument. Argentina, 2008: the entire private pension system seized in a week. And the most instructive case ran both experiments at once — Alaska constitutionalized its corpus in 1976 and left the dividend formula in statute; fifty years on, the corpus has never been touched and the dividend has been a political football since 2016. Constitutional pile, statutory payout: the pile survives, the payout gets eaten. Norway's fiscal rule, by contrast, is a norm sustained by consensus culture and would last one American election cycle; Social Security's protection is political, not legal — Flemming v. Nestor holds there is no property right in benefits at all. Statute is sand. Norms are fog. Only text plus vested title is rock.

Hence the Keel. Title never sovereign: purchases convey to individual citizen accounts at settlement; the state is a buying agent, never an owner, so there is no pool to seize — only three hundred forty million individually titled holdings, each raid a compensable taking with a named plaintiff. Purchases on ministerial autopilot: formula-mandated, cap-weighted only; no official may direct, pause, tilt, or target a purchase, so no industrial-policy lever exists to capture. The payout formula in the constitutional text — the Alaska lesson — at the same altitude as the length of a Senate term. Voting mirrored or passed through to citizens, with a constitutional bar on bloc voting at any official's direction: the fund can never be aimed, by either party, in either direction — which also dissolves the one documented pathology of universal ownership, the common-ownership competition-softening effect, because when the shareholders are the customers, the softening incentive inverts. Universal standing: any account holder may sue over any deviation, and the fund's ledger is append-only, replayable, and public — determinism as constitutional armor; any citizen can replay the fund's entire history and prove a deviation in court. And asymmetric entrenchment: the invariants — universality, per-capita equality, inalienability, mirrored voting, never-sovereign title — absolute; the parameters — rates, thresholds, payout percentages — adjustable within written corridors by supermajority. Correctable where it must bend; unbreakable where it must not.

One clause is pure political engineering and may matter more than all the law: the fund reports in units, not dollars. Social Security survives drawdown politics because no one marks their future benefits to market. The Birthright statement says: your daughter owns 214 units of American enterprise, up 31 this year — a number that, by construction, only rises, and rises fastest in crashes. The profit-and-loss lives in an actuarial appendix. Bogle spent fifty years telling investors to count shares and ignore quotes; the fund is constitutionally required to talk like him.

And the deepest armor is not in the text at all. It is the bet the whole design rests on: that an eighteen-year-old holding three hundred thousand dollars of the American public markets will like it — really like it — more than the seductive words of any populist, left or right. That bet has receipts. Postwar land reform in Japan, Korea, and Taiwan was executed explicitly to create owner classes that would never go communist, and it built three durable democracies. Thatcher's Right to Buy moved a million tenants measurably toward the politics of property. The demagogue's fuel is assetlessness — "the system is rigged" is not a hypothesis to a twenty-four-year-old with debt and no assets; it is an accurate reading of their balance sheet. Hand the same speech to a room where every listener holds titled units and let me tear it down parses as let me tear down your net worth. You have not out-argued the demagogue. You have repossessed his audience. The one cautionary twin is Chile, whose private pension system should have built exactly this constituency and instead became the target of the 2019 uprising — because intermediaries skimmed fees for decades. In this design, Bogle-cost is a survival requirement, not a preference: the moment a manager class is seen farming the birthright, the constituency flips from defender to mob. The Keel's no-manager, cap-weighted autopilot exists because of Santiago.

Name the aim precisely, because "weaken populism" is the confession my enemies would quote for fifty years. Populism is two forces wearing one name. The corrective demand of the governed — Machiavelli's people, who desire merely not to be oppressed — is the political immune system, and this design depends on it; the Keel is nothing but organized rock-throwing capacity. The target is the second force: the demagogic monetization of despair, the entrepreneur of grievance who harvests assetless rage into unaccountable power, after which the extraction resumes under new management. That force is fuel-limited, and the only regimes that ever actually killed a populist wave did it by delivering the populists' legitimate demands before the demagogue could cash them — Bismarck's pensions, FDR's hundred days. The formulation: starve the demagogue, arm the citizen. The same act does both. And to the bread-and-circuses attack, the distinction that holds: circuses are flows from the ruler, revocable, aimed at spectators. Title creates principals. Rome's mob held grain at the emperor's pleasure. The eighteen-year-old holds units no emperor can touch, and a cause of action if one tries.

There is a military corollary, and it is not a digression. America already runs a social wealth fund for the assetless — it is called enlistment, and it charges bodies as the admission fee. The country ran both arms of the experiment on the same cohort, and the first arm deserves more than a sentence, because you were almost certainly never taught it. In the summer of 1932, more than forty thousand veterans of the First World War and their families — men holding government service certificates they could not redeem until 1945, men who had been promised a bonus for their service and handed an IOU into the teeth of the Depression — marched on Washington and built a shantytown on the Anacostia flats to petition for early payment. The Senate voted them down. On July 28th, President Hoover sent the Army against its own veterans: Douglas MacArthur commanding, George Patton leading the cavalry, Dwight Eisenhower as his aide — three future legends deployed with tanks, sabers, and gas against men wearing the same medals they wore. The camps were burned to the ground. Veterans died. It remains the only time in American history that the Army made war on its own soldiers in the capital, and it is strangely absent from the curriculum — I am an educated man and no school ever mentioned it to me. Draw your own conclusions about who writes curricula and which precedents they prefer forgotten. Twelve years later, the planners of the GI Bill wrote with Anacostia explicitly in mind — the legislative record says so — and chose the opposite policy: sixteen million returning soldiers handed education and zero-down mortgages, producing the most stable, civic, institution-trusting generation in American history. Same demographic, same war-forged men; the variable was title. The GI Bill was a birthright fund with a four-year enlistment as the price of admission. This design unbundles the stake from the rifle — and in doing so completes Kant, whose republican peace assumed citizens bear war's costs, an assumption modern deficit finance and a poverty-recruited force quietly broke. A nation where every household holds the index re-couples war's costs to the electorate's quarterly statement. The volunteer who serves anyway, holding a portfolio, was always the republican ideal. The racket only ever worked on those who had no other door.

X. The Evidence

The fertility claim is the masthead and the most attackable link, so it gets stated as what it is: a calibrated hypothesis with a falsifiable prediction, not a promise. But the calibration is far stronger than the baby-bonus debate knows, because the empirical literature has accidentally run the decisive experiment — stock versus flow — and the stocks win.

The flows first, with their limits in view. Quebec's Allowance for Newborn Children: an extra thousand Canadian dollars raised fertility roughly seventeen percent (Milligan 2005). Spain's baby check: introduction raised births three percent — and cancellation cut them six, the revocation destroying more births than the grant created, which is the empirical fingerprint of why flows are inferior (González 2013; González and Trommlerová 2023). Israel's child allowances: benefit elasticity around 0.19 (Cohen, Dehejia, and Romanov 2013). A German welfare cut of eighteen percent of household income reduced fertility about seven percent. Real, dose-responsive in both directions, and mortal with the budget. The standing cautions: Korean baby-bonus work finds over ninety percent of lump-sum spending goes to infra-marginal births, and Kearney and Levine's post-2008 work shows much of the American decline is priorities, not prices — the cultural ceiling on any financial lever. Hungary spent on the order of five percent of GDP in pro-natal flows for roughly plus 0.2 TFR, revocable every budget.

Now the stocks. Lovenheim and Mumford (2013), the cleanest asset shock in the literature: one hundred thousand dollars of housing wealth caused a sixteen-to-eighteen percent increase in the probability of a birth for owners — and zero effect on renters facing identical prices. Holding the asset is the mechanism. Russia's maternity capital — a restricted-use capital grant, the closest existing policy to an unstrippable stock — raised total fertility with large general-equilibrium effects (Malkova 2018; Yakovlev and Sorvachev 2020). Brazilian housing-credit lotteries provide causal evidence that housing access itself moves fertility (van Doornik et al. 2025). And the closest structural analog to the Fund that has ever run is Alaska: a permanent, universal, constitutionally protected dividend from an owned fund raised fertility 13.1 percent against a synthetic control from 1982 to 1988 — strongest among women thirty-five to forty-four, with no change in teen births or abortion: planned completions of deferred families, the confidence signature — with one follow-on estimate attributing plus 0.59 TFR across 1982 to 1995 (Yonzan, Timilsina, and Kelly 2023).

Sort the entire literature by instrument type and the pattern is unmistakable: permanent, owned, unrevocable claims show the largest and most durable effects, and the one observed revocation destroyed more than the grant created. The evidence-grounded band for the combined design — accounts of one hundred fifty to three hundred thousand dollars at childbearing age, plus a permanent stewardship dividend at post-buyback-ban yields — runs from roughly plus 0.1 TFR at the conservative floor to plus 0.6 at the Alaska long-run bound. On America's 1.62, the middle of that band reaches toward 1.9; the top brushes replacement. [Fig. 3, Section III, carries all four calibrations as cited presets — pick a paper, inherit its assumptions.]

The straight version for the skeptic: no economy has run this at scale, and the gap between desired and achieved fertility in American surveys — roughly half a child per woman — is the precisely measured size of the target. This design does not promise to make people want children. It promises to stop charging them rent on wanting what they already want. If TFR has not moved by year ten, the fertility hypothesis is falsified — and the country still holds the fund, the floor, the clean profit ledger, and the de-captured market. The plan is convex to its own most uncertain claim.

There is also a spatial multiplier the calculators undercount. Every benefit in the stack is flat, federal, and nominal, while the cost of deploying dollars varies threefold across American geography — so the design is a real-income gradient pointing away from the megacities. Twenty-five thousand dollars of household capital income is a rounding error against coastal rent and a paid-off homestead with margin for a third child in a hundred-forty-thousand-dollar-house county. For the first time since industrialization, the Zipf ladder has a down escalator that pays — and it is landlord-proof by geometry, because only in supply-elastic geography does the benefit escape capitalization into rents. Since rural fertility already runs 0.3 to 0.5 above dense-urban fertility, migration down the cost gradient raises national fertility by pure composition before any treatment effect fires. The graveyard finally has a counterweight. And the same gradient is the ratification map: the amendment needs thirty-eight states, the Senate is malapportioned toward exactly the states where flat federal dollars buy the most, and the plan is therefore — for once — shaped like the Senate. The largest de facto rural development program in American history, passed without ever containing the word rural.

XI. The Objections

The strongest opposition memo writes itself, and a plan is only as good as its answers.

You built the largest political weapon in history — a fund owning a quarter of corporate America. Answered structurally, not rhetorically: the fund as a discretionary pool never exists. Title conveys to citizens at settlement; purchases are ministerial and cap-weighted; votes are mirrored or passed through; the ledger is public and replayable; every citizen has standing. There is no chair of the fund, no number to call, and nothing to capture but a formula. The residual risk — a regime that ignores text — is answered by the constituency, which is the point of the whole design.

The carry trade blows up in a lost decade. The state already runs the trade with the legs reversed — short the put, long nothing — and loses every crisis by construction. The covered version cannot be margin-called, buys most when prices are lowest, and reports in units that rise fastest in crashes. Sequence-of-returns risk is real and is answered by sizing, infinite duration, and the units accounting; it is not answered by pretending the current naked-put position is safe.

The transition costs a trillion a year. The gap is two decades of a declining-quality tax swapped for a perpetual compounding claim that ends larger, financed by issuance the mechanism already contemplates, partially self-offset by the repricing the policy itself causes — and the answer to bond-market discipline is to start smaller than one percent and sequence in the open: buy first, cut later, scale with credibility.

Fission disarms America against China. Champions don't innovate; escapees do — the transistor had to be pried out of Bell by a consent decree to become Silicon Valley, and the transformer had to flee Google to become the AI boom. China's fearsome sectors were forged by domestic hyper-competition, not consolidation. Fission multiplies American shots on goal and produces allied fleets, not fragments.

The kill-zone ban murders venture exits. The behavioral refinement — bar acquisitions that discontinue the product, keep the sub-hundred-billion buyer pool rich, revive the IPO channel with the zero-tax listing magnet — targets the five-to-seven percent of deals that are killers without executing the rest.

Hayek: half the market held by permanent capital destroys price discovery. The design adds discovery organs the current passive regime lacks: the fund as the market's great securities lender, subsidizing the shorts who keep prices honest, with lending revenue flowing to the birthright accounts; a seasoning rule keeping the fund out of IPOs and first-year listings so every new company prices against elastic capital; the tithe and the step-up repeal as standing sell-side pumps unfreezing trillions in locked float; and the Ladder generating forced repricings with every fission. The plausible end state has more price discovery than today's market, where the Big Three neither lend strategically, nor abstain from new issues, nor break anything apart, nor pass a dollar to the median household.

The fertility promise will fail and discredit everything. It is published as a hypothesis with a prediction and a falsification date, chained to nothing else in the design — every other organ stands on its own returns.

XII. The Settlement

Step back and look at the physiology, because this stopped being a list of policies somewhere around the fourth mechanism. Corpus untouchable at the bottom — the birthright and the hearth. Transparency mandatory in the middle — the ten-billion door. Fission automatic at the top — the trillion-dollar blade. Surplus routed as dividends into households instead of locked paper. Innovation routed as competition instead of consumption. A two percent osmotic gradient pulling ownership from peaks to floors through a fund that buys every month forever, whose title rests in three hundred forty million accounts, denominated in units that only go up. It is a circulatory system, and every organ answers a documented failure: Russia's vouchers, Hungary's raid, Chile's fees, Alaska's clipped dividend, Japan's zombie holdings, the Bell Labs warehouse, the kill zone, the Anacostia flats.

The passive-index revolution already proved the machinery works — it built a permanent universal bid and a universal owner, and then installed the wrong beneficiaries and concentrated the votes in three buildings. Everything tragic about indexing is a title problem and a plumbing problem. None of it is physics. Bogle built the structure and spent his final years warning about the concentration; he did not live to propose the fix. This is the fix, offered as a memorial: finish the mutualization — extend Vanguard's ownership structure past the fund industry to the market itself, past the saving class to every birth certificate, and shard the votes he feared. Make everyone a Bogle.

And the reason to do it is the one this essay opened with. The attractor is real, it is visible, and visibility has not saved a single country from it — because lucidity without a mechanism is just watching. The extraction that feeds it has a face now, and it is not the founder's or the engineer's or even the working billionaire's: it is the toll booth. The low-effort elite have been consuming our future children — not as metaphor but as measurable incidence: housing speculation pricing out the nursery, credential tolls consuming the fertile decade, buybacks locking the surplus away from kitchens, debt peonage making the eighteen-year commitment an unbounded downside, and a demagogue class harvesting the resulting despair. Every gap between the families Americans say they want and the families they have — half a child per woman, the largest measured theft in the country — is the invoice.

The demagogue's pitch has always been the same: only I can give you back what they took. The Birthright answer is shorter, and it fits on a chit, and it compounds quarterly:

It's already in your account.

Epilogue: The Kitchen, Again

Run the scene once more, in the other world.

The garage at 4:40. The badge already dead on the lanyard — they still do that; no law reaches every indignity. Eleven years, and the org is still flattening, and he still can't finish the sentence about synergies, and it still feels like being told a decade of your life meant nothing. The Fund does not fix that. Nothing fixes that.

But the folder on the table is a different folder. Her statement — units, up again this year, the way the number is always up, because it is a count and not a price. His. The mortgage on a house that owes the county nothing, because it is a hearth below the line. And the deposit that arrived on the first, the way it arrives every first, paid out by the machine that just took his job — because he owns a piece of the machine that took his job. So does she. So will the child, from the day there is a birth certificate: an account no layoff, no lender, no bad year, no bad man can ever touch.

He is still ashen. She still sees it, and it still breaks her heart a little, and the dinner they are about to have will still be hard. But she has done this math too. Nine times.

This time it is close enough to argue with.

She takes the test out of the drawer.

Model notes, effect sizes, and all cited calibrations are interactive in Figure 3. The mechanism is on the shelf. — E.B.

Sources & References

Demography & history

- UN DESA — World Population Prospects 2024, Summary of Results

- Our World in Data — fertility above/below replacement, by country

- Statistics Korea (via Korea Herald) — TFR 0.72, world's lowest (2023)

- Seoul total fertility rate ~0.55 (Statista)

- The urban graveyard effect — demographic history of cities

- Wrigley — "A Simple Model of London's Importance…," Past & Present (1967)

- Taub Center — Israel's exceptional fertility

- CDC QuickStats — US fertility by urbanization level

- The Bonus Army (1932)

- The G.I. Bill (1944)

- US State Dept — occupation land reform in Japan, 1945–52

- Right to Buy (Housing Act 1980)

- CFR — Chile's pension system and the 2019 uprising

- Social Security Administration — Otto von Bismarck's social insurance

- Reform Act 1832

- Reform Act 1867

- Share Our Wealth — Huey Long (1934–35)

- Stanford Encyclopedia — Kant's political philosophy and Perpetual Peace

- Hume — "Of the First Principles of Government"

- Hardin — "Why a Constitution?" (constitutions as coordination)

- Machiavelli — Discourses on Livy, I.5

- Alaska Constitution, Article IX §15 (the Permanent Fund)

- ADN — Gov. Walker caps the PFD (2016)

The fertility literature

- Milligan — "Subsidizing the Stork," Review of Economics and Statistics (2005)

- González — Spain's universal child benefit, AEJ: Economic Policy (2013)

- González & Trommlerová — cancellation effects, Journal of Human Resources (2023)

- Cohen, Dehejia & Romanov — "Financial Incentives and Fertility," REStat (2013)

- Riphahn & Wiynck — "Fertility Effects of Child Benefits" (IZA DP 10757)

- Korean baby bonus — reservation price of fertility, Economics & Human Biology (2021)

- Kearney, Levine & Pardue — "The Puzzle of Falling US Birth Rates," JEP (2022)

- AEI — Hungary's ~5%-of-GDP pro-natal spend and its limits

- Lovenheim & Mumford — housing wealth shocks and fertility, REStat (2013)

- Malkova — Soviet maternity benefits, REStat (2018)

- Yakovlev & Sorvachev — Russia's maternity capital, long-run effects (SSRN)

- van Doornik, Gomes, Schoenherr & Skrastins — "Housing and Fertility" (BCB WP 612)

- Yonzan, Timilsina & Kelly — Alaska's PFD and fertility (NBER WP 26712)

- CDC/NCHS QuickStats — expected lifetime births, US 1940–2018

- Gallup — Americans' ideal family size (~2.7)

- Badolato — "The fertility desires–intentions gap in the United States," Population Studies (2025)

- Federal Reserve — Distributional Financial Accounts (top 10% hold ~88% of equities)

- Bebchuk & Hirst — "The Specter of the Giant Three" (NBER WP 25914)

- Johansson et al. — "Taxation and Economic Growth" (OECD WP 620)

- Lucca, Nadauld & Shen — "Credit Supply and the Rise in College Tuition" (NY Fed SR 733)

- Perry (AEI) — cosmetic-procedure prices vs. insured medicine

- USDA — Expenditures on Children by Families

Financial precedents & market structure

- Japan Times — the BOJ's ¥83T+ ETF holdings and sell-down plan (2025)

- Norges Bank Investment Management — ~1.5% of the world's listed companies (official)

- HKMA (Norman Chan) — the August 1998 stock market operation, HK$118B

- Tracker Fund of Hong Kong — the 1999 disposal to citizens

- James Meade — property-owning democracy and the social dividend

- U.S. Treasury — TARP (official)

- Federal Reserve — Secondary Market Corporate Credit Facility, 2020 (official)

- FHFA — the Fannie Mae & Freddie Mac conservatorships (official)

- U.S. Treasury — final AIG sale, $22.7B positive return (official)

- St. Louis Fed — the 2020 emergency facilities wind-down

- Mariana Mazzucato — The Entrepreneurial State

- SEC — Rule 10b-18 buyback safe harbor (1982)

- S&P Dow Jones Indices — S&P 500 buybacks set a $942.5B record in 2024

- Cunningham, Ederer & Ma — "Killer Acquisitions," Journal of Political Economy (2021)

- Kamepalli, Rajan & Zingales — "Kill Zone," NBER WP 27146

- Watzinger et al. (CEPR/VoxEU) — the 1956 Bell consent decree and innovation

- The breakup of the Bell System (1984)

- The Traitorous Eight — Shockley → Fairchild → Intel

- "Attention Is All You Need" (2017) — all eight authors have left Google

- Arrow (1962) and the replacement effect (Shapiro)

- Mancur Olson — The Logic of Collective Action

- Gilens & Page — "Testing Theories of American Politics," Perspectives on Politics (2014)

- SIFMA Fact Book — U.S. equity market capitalization (~$62T)

Law & policy

- Voucher privatization in Russia, 1992–1994 (Wikipedia)

- Homestead Acts (Wikipedia)

- Dawes Act of 1887 (Wikipedia)

- Spendthrift trust (Cornell LII Wex)

- 29 U.S.C. §1056 — ERISA anti-alienation (Cornell LII)

- 42 U.S.C. §407 — Social Security anti-assignment (Cornell LII)

- Flemming v. Nestor, 363 U.S. 603 (1960)

- Double Irish arrangement (Wikipedia)

- Ireland's 12.5% corporation tax (Wikipedia)

- Delaware Division of Corporations — Fortune 500 statistics (official)

- OECD Pillar Two global minimum tax (Wikipedia)

- 26 U.S.C. §877A — expatriation exit tax (Cornell LII)

- Stepped-up basis and buy-borrow-die (Wikipedia)

- Switzerland's cantonal wealth tax (Wikipedia)

- Hungary's 2010–11 pension nationalization (IPE)

- Poland's 2013 pension bond transfer (EBRD)

- Argentina's 2008 AFJP nationalization (Global Voices)

- Norway's fiscal rule — handlingsregelen (Wikipedia)

- Alaska Permanent Fund Corporation — official history

- John C. Bogle (Wikipedia)

- Vanguard's mutual ownership structure (official)

- California "data dividend" proposal, Newsom 2019 (CNBC)

- Georgism (Wikipedia)

Compiled July 2026. Interactive calibrations and model notes: Figs. 1–3. Plate sources are printed on each plate.

Related Posts

The Birthright Fund in Five Minutes

The five-minute version: buy 1% of the market every year forever, convey it to every birth certificate, lock it for life — six mechanisms, the precede...

Story Is the OG Intelligence Technology

Why a podcaster gets paid more for chatting with a scientist than the scientist gets paid for the breakthrough. The economy isn't broken — it's revert...

The Price of Tomorrow: $355 Billion and a Prayer

Four labs. $355 billion in committed 2026 capex. One spreadsheet error from bankruptcy. I built a game to let you feel what it’s like to bet the compa...

Subscribe to the Newsletter

Get notified when I publish new blog posts about game development, AI, entrepreneurship, and technology. No spam, unsubscribe anytime.

Comments

Loading comments...

Published: July 11, 2026 7:54 PM

Last updated: July 11, 2026 7:54 PM

Post ID: 2b4b5e2f-d8ea-4b49-b1d3-18d4e3cf596a