Lex SpaceX: Two Index Giants Bent the Rules for SpaceX — the Biggest Refused

Nasdaq, S&P, and FTSE Russell rewrote their rulebooks so passive money must buy SpaceX at a price it had no hand in setting. My lens, on the record before the June 12 bell, with six falsifiable predictions.

Share this post:

Export:

I am going to be as direct as I know how to be, and I am going to do it before June 12, when the SpaceX IPO prices and the facts are still unknown, because a thesis is only worth something if you state it before the dice land.

Here is the claim. Price formation at the top of the US market is no longer mostly price discovery. It is mostly forced buying. Cap-weighted passive flows push a disproportionate share of every indexed dollar into the largest names, mechanically, with no reference to value — and that mechanism, not fundamentals, is now the dominant force setting megacap prices. I have argued this throughout this series as an inference from the math. The SpaceX IPO is the moment the mechanism stopped being an inference and became a confession, because to pull it off, the index providers were pushed to rewrite the written rules — the seasoning periods, profitability tests, and free-float minimums that have governed inclusion for decades. Nasdaq and FTSE Russell bent; S&P Dow Jones proposed to, then, on June 4, refused (see the update above). The German press named the pattern with a precision the American press dodged: Lex SpaceX. A law written for one company — and, at one index, a law the keeper declined to write.

This is the cleanest real-world proof of the SP3 thesis I will ever get, and it is happening in public, on a known date. So I am planting my flag now.

A rule of thumb to keep in your pocket. Each 1% of the S&P 500 you occupy is worth roughly $130 billion of one-time forced buying the moment index funds have to hold you — and about $300 million more every month after that, bought automatically, regardless of price. The whole SpaceX rule fight came down to one question: is SpaceX's slice measured at ~0.1% (its actual tradable float) or juiced toward its headline weight? The providers just answered it differently — Nasdaq and Russell yes, the S&P 500 no (see the update above) — which is why the near-term forced buying lands in the Nasdaq-100, not the flagship index. The rules decide the size of the bid. The full arithmetic is in the sidebars below.

The offering

The facts of the offering, as priced on the roadshow:

- Listing: Nasdaq, scheduled June 12, 2026.

- Price: a fixed $135 per share.

- Valuation: roughly $1.77 trillion — which would make SpaceX about the seventh-largest US company by market cap on day one, above Tesla.

- Raise: 555.6 million shares for roughly $75 billion, with an underwriter over-allotment of another 83.33 million shares (~$11.2 billion). Goldman Sachs leads, with Morgan Stanley, Bank of America, Citigroup, and JPMorgan.

- Control: Musk retains over 82% of voting power through super-voting stock, while holding only about 12.3% of the Class A economic shares.

- Float: the genuinely tradable float is estimated at only 3–5% of the company. At a ~$1.77T valuation that is on the order of $50–90 billion of actual shares — a rounding error against the index money about to be pointed at it.

Hold those last two numbers together: a company that will be one of the seven biggest in America by index weight, with a tradable float of a few percent, controlled entirely by one person. That combination is precisely what every inclusion rule on the books was designed to keep out of a passive portfolio. So the rules were changed.

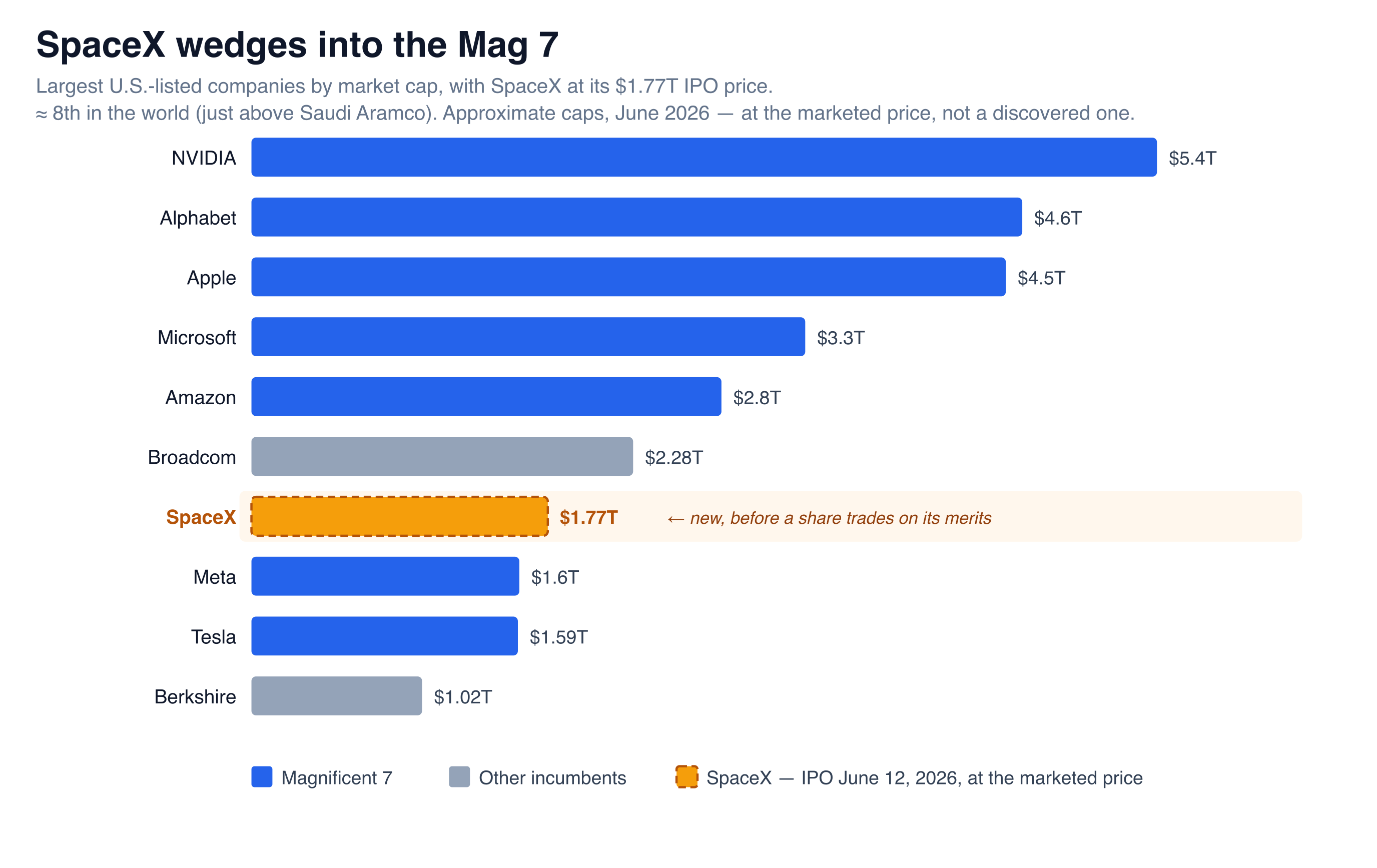

The chart leading this piece ranks them. At $1.77 trillion, SpaceX would be the eighth-most-valuable company on Earth the instant the bell rings — wedged onto the lower edge of the Magnificent 7, above Meta and Tesla, behind only Nvidia, Alphabet, Apple, Microsoft, Amazon, Broadcom, and (by a $10-billion hair) Saudi Aramco. Counting US-listed names only, it is seventh. Sit with what that means: it is not the eighth-biggest company because eight markets' worth of buyers weighed it against the alternatives and arrived there. It is the eighth-biggest because a fixed offer price was multiplied by a share count, and a forced index bid is being arranged to meet that price. Morningstar pegs fair value at less than half. A genuinely floated, price-discovered SpaceX might rank fifteenth, or twentieth, or lower — we will never find out, because the structure is built precisely so that we don't have to.

The three rewrites

Nasdaq — the "Fast Entry" rule (enacted). Nasdaq circulated a consultation in February 2026, closed comments on February 27, and made the rule effective May 1, 2026. It creates a fast-entry path for companies that would rank near the very top of the index (reported as roughly the top 40 by market cap): inclusion in the Nasdaq-100 just 15 trading days after IPO, versus the historic three-month seasoning period. It also abolishes the 10% minimum free-float requirement for these names, and lets low-float companies be weighted at an inflated multiple — up to 3× their actual float — phasing the weight up over time. Because fast entry does not bump an existing member out, the index can temporarily hold more than 100 constituents. Per Reuters' sources, early index inclusion was a stated condition of SpaceX choosing Nasdaq over the NYSE. Projected Nasdaq-100 entry is around July 7, 2026.

S&P Dow Jones — proposed, then refused. S&P opened a consultation (April 30–May 28) on whether to cut the seasoning period from 12 months to 6, waive the profitability test (the decades-old four-consecutive-quarters-of-GAAP-earnings rule), and waive the 0.10 Investable Weight Factor float minimum for "MegaCap" companies (reported threshold ~$112 billion). On June 4 it gave its answer: no. It reaffirmed all three requirements for the S&P 500, the MidCap 400, and the SmallCap 600, ruling that "exceptions … should not be granted solely based on market capitalization." SpaceX — unprofitable and thinly floated — now waits a year or more for the flagship index; S&P will admit it only to its broader, far-less-followed S&P Total Market and Dow Jones U.S. Total Stock Market indexes. The most-watched index in the world held the line.

FTSE Russell — changed. Russell did bend, and harder than Nasdaq on timing: it shortened post-IPO inclusion to as little as 5 trading days, opening a Russell-index pathway within a week or two of listing.

The lockup was engineered to feed the machine

The float problem had a second solution, and it is the tell. A normal IPO locks insiders up for 180 days. SpaceX instead built a tiered set of release valves: after its first quarterly report as a public company, insiders may sell up to 20% of eligible locked shares; another 10% if the stock trades 30% above the IPO price on at least 5 of the 10 trading days after that report; and 7% tranches at 70, 90, 105, 120, and 135 days post-IPO. Musk himself is exempt from these early-release provisions.

Read that as what it is: a schedule designed to manufacture tradable float quickly in the weeks after listing — which is exactly what is needed to satisfy float-based index weighting and accelerate inclusion. The lockup is not a constraint on the index play. It is a component of it.

Why this is inorganic, precisely

When an index adds a name, every fund tracking that index must hold it at its target weight. To buy it, the funds sell proportional slices of everything they already own — Apple, Microsoft, Nvidia, Amazon and the rest get trimmed to raise the cash. None of this buying expresses any view about SpaceX. It is mechanical, it lands in a concentrated window, and it pays whatever the price is at the moment of inclusion.

The float multiplier makes it worse. Weighting a 3–5%-float company at up to 3× its float means index demand is sized to a share count that does not tradably exist, concentrating mechanical buying into a thin book. That is the textbook setup for the price to be pushed up into inclusion and to sag after it, once the forced bid is spent — which is precisely the pattern the academic work predicts.

Murray and Sammon (2026) find that short five-day seasoning windows cause prices to rise ahead of inclusion and then fall by as much as 10% afterward, with index investors forced to buy at the inflated level — while issuers raise about 6% more capital for the privilege. The long seasoning period exists for a reason: it lets arbitrageurs accumulate gradually and spread the price impact out, protecting the passive holder. Shortening it transfers money from the index investor to the issuer. The precedent everyone cites is VinFast (August 2023): listed with a ~1% float, it spiked roughly 700% to a near-$200B valuation that one analyst called "bafflingly overpriced," then collapsed from about $17 to $3.

The numbers — honestly, because the honesty is the weapon

Here is where this story is most often abused, so I will be exact and I will show the disagreement rather than hide it. Estimates of the forced buying span more than an order of magnitude, because the answer depends almost entirely on the float-multiplier assumption:

- Nasdaq's own estimate: about $6 billion of mechanical demand, against roughly $600 billion in Nasdaq-100-tracking products.

- Independent desk estimates (SpotGamma and others): roughly $7B+ forced single-day buying in QQQ and $8–12B+ across S&P 500 trackers, for a combined ~$15–30 billion across the S&P 500, Nasdaq-100, and Russell 1000 families under conservative weighting — escalating sharply under aggressive float multipliers, with a tail scenario near $200 billion if full multiplier weighting were applied across ~$11T of S&P-linked assets.

- Goldman Sachs (per Fortune): as much as $60 billion of forced buying across the Nasdaq-100 alone — far above Nasdaq's own figure.

The spread between $6B and $60B for the same index is not noise to be averaged away. It is the story: nobody actually knows, because the weighting rules are new and the float is being manufactured on a schedule, and a structure whose forced demand can be credibly estimated anywhere from single-digit to sixty-plus billion dollars is a structure with no price discovery in it at all. One distinction is worth holding onto, because it is where most scare numbers go wrong: the figure that matters is the inclusion trade — the shares index funds must actually buy — not the pool of money indexed to the benchmark. The pool is measured in tens of trillions; the trade, even in the aggressive scenarios, in tens of billions. Quote the trade, not the pool.

Sidebar 1: what a slice of the index is actually worth

Let me turn the mechanism into a number you can carry around. The inputs, all sourced and all order-of-magnitude (flows move month to month — treat these as a napkin, not a model):

S&P 500 total market cap ≈ $65T (2026)

Passively indexed to it ≈ $13T (≈ $20T benchmarked) — S&P DJI, Feb 2026

Net inflows to S&P 500 vehicles ≈ $20–40B / month (est.)

VOO alone took $137.7B in 2025 ≈ $11.5B/mo — one fund

KEY: index weight is FLOAT-ADJUSTED market cap, not headline cap

Two entitlements fall out of this, and they are different animals:

The one-time entitlement (joining, or stepping up in weight). When you reach a given index weight, every passive fund must buy you up to it at once.

one-time forced buy ≈ your weight × $13T→ 1% of the index ≈ ~$130B that must be bought. Each 0.1% ≈ ~$13B.

The recurring entitlement (the perpetual drip). Every month, new money flows in and buys you at your weight, forever, regardless of price.

monthly forced buy ≈ your weight × ~$30B/month of inflows→ 1% of the index ≈ ~$300M of automatic, price-insensitive buying every month. A 7% giant ≈ ~$2B/month.

The catch — and it is the whole catch — is the word float-adjusted. Your entitlement is computed on the shares actually available to trade, not your headline valuation. That single word is what the spring 2026 rule changes went after. Waiving the 0.10 float minimum and allowing up-to-3× float weighting doesn't change your company; it changes the number your entitlement is multiplied against. The rule fight is not abstract governance. It is a fight over the size of a guaranteed bid.

Sidebar 2: the napkins behind the curtain

Once you see the two entitlements, you can run the same arithmetic the principals are running.

The napkin Elon's bankers are running. SpaceX at $1.77T is ~2.7% of a ~$65T index by headline cap. But its tradable float is only 3–5% — call it ~$70B — so by the old float rule its weight is closer to ~0.1%. Watch what that does to the one-time forced buy:

Float-adjusted (old 1× float rule): ~0.1% × $13T ≈ $13B

Up-to-3× float multiplier (new): ~0.3% × $13T ≈ $40B

Full-cap weighting (hypothetical): ~2.7% × $13T ≈ $350B

That spread — roughly $13B to $350B — is not an accident of estimation. It is the prize. Every rung up that ladder is a rule concession, and each one is worth tens to hundreds of billions of dollars of buying that arrives no matter what the company is worth. The bankers' napkin is brutally simple: lobby the index committee for the highest weighting treatment you can get, then harvest the spread. The IPO price is almost a detail next to which rung you land on.

The napkin Apple's or NVIDIA's CFO is running. Now flip to the incumbent's seat, designing next quarter's capital return. You already sit at ~6–7% of the index, so the perpetual drip hands you, free, on the order of ~$2B/month of automatic buying. Then you stack your own price-insensitive bid on top:

Free index drip (≈7% × ~$30B/mo) ≈ $2B / month

+ Apple buyback ($100B/yr authorization) ≈ $8B / month

(or NVIDIA: +$60B in 2025; ~$52B repurchased over 12 mo ≈ $4B/mo)

= price-insensitive demand against your stock ≈ $10B / month

That is not "returning capital to shareholders." That is engineering the bid. And the dividend is the second instrument: initiate or sharply raise it and you convert growth holders, who rotate, into income-mandated holders, who cannot. The CFO's real quarterly question is not "are we undervalued?" It is: how much buyback do I layer on top of the free index drip to defend or extend my weight, and when do I switch on the dividend to bolt the holders down? Once you are big enough, your market cap is partly a thing you operate, not only a thing the market discovers.

(All figures above are sourced order-of-magnitude estimates; monthly flows are volatile and the weighting outcomes depend on the rules. The arithmetic is shown precisely so you can redo it with better inputs.)

Sidebar 3: NVIDIA just ran the CFO napkin in public

You do not have to imagine the incumbent's playbook — NVIDIA executed it, line by line, in its most recent quarter (Q1 of fiscal 2027, reported May 2026). Alongside record revenue of $81.6 billion (up 85% year over year), the company:

- added $80 billion to its buyback authorization — pushing total repurchase capacity to roughly $120 billion;

- raised its quarterly dividend from $0.01 to $0.25 a share — a 2,400% increase, i.e. 25×; and

- returned about $20 billion to shareholders in the single quarter.

Read through the lens, neither headline move is quite what its label says.

The $80B is the engineered bid. Twenty billion returned in one quarter is roughly $7 billion a month, the bulk of it repurchases — a price-insensitive bid NVIDIA points at its own stock, on top of the free index drip it already collects as the single largest weight in the S&P 500 (~8% → on the order of $2B+/month). Stack them and you get a self-directed bid in the neighborhood of $7–9 billion a month, with ~$120B of authorized dry powder behind it, that has nothing to do with whether NVIDIA is a good buy this month.

The 25× dividend is not about income — the math gives it away. A dollar a year on a roughly $220 stock is a yield of about half a percent. No income investor is buying NVIDIA for 0.5%. So why initiate a real dividend at all, when the company has thrown off excess cash for years? Because the move is a category switch, not a payout. Going from a token penny to a committed quarter-dollar flips NVIDIA from a pure growth name — which rotating growth holders sell when momentum cools — into a dividend-paying staple that income-mandated funds and dividend indices can, and in some cases must, hold. The 25× is not paying you. It is broadening and bolting down the holder base, and signaling permanence to the holders already there. The tell is the timing: you switch the dividend on when you want to lock the float, not when you happen to have spare cash.

That is the CFO napkin, executed: a free index drip, plus an $80-billion self-directed bid, plus a dividend engineered for lock-in rather than yield. NVIDIA is not returning capital. It is operating its market cap.

And the timing is its own disclosure. Be careful with the cynical read here, because the obvious version is wrong: this is not a company whose growth has stopped — revenue was up 85%, data-center nearly doubled. The exponential is still firing. Which is exactly why reaching for the toolkit now is the tell. You do not bolt down your holder base with an income mandate, or commit to a sticky dividend you can never cut, while you genuinely believe the growth will keep holding them for you — you do it when you can see, before the market prices it, where the curve bends. A committed dividend is a statement about durable cash flow, not continued hypergrowth; those are different bets, and NVIDIA just quietly placed the first one. So read it not as a growth obituary but as deceleration insurance, bought while the cash gusher makes it cheap: NVIDIA did not announce that the exponential is ending, it allocated as if it eventually will — which is a more honest disclosure than anything in the press release. (The honest caveat: capital allocation is a noisy signal of intent, and the new index rules make "operate your market cap" attractive for every top name right now — so some of this is NVIDIA reading the changed game, not only its own curve.)

Sidebar 4: should you trade around the inclusion? No.

A fair question, once you see that index funds will trim the giants to fund SpaceX: if you hold those giants, should you sell ahead of the rebalance and buy back cheaper? Almost certainly not — and the reasons double as a lesson in how small these flows are per name.

If you hold the shares outright, you are not funding anything. The reallocation is done by index funds trimming their holdings. Your shares are not in anyone's rebalance basket; the funds sell the same amount whether you hold or not. You cannot opt out of someone else's rebalance by selling your own stock.

The per-name drag is a rounding error. A ~$10B inclusion buy, funded pro-rata, lands maybe ~$2B of selling across the top names — against ~$14 trillion of their combined market cap, that is one or two hundredths of a percent, once, and it is already front-run because the date and the flows are public.

The round-trip cost dwarfs the wiggle. In a taxable account, selling a position held under a year realizes short-term gains taxed as ordinary income — a real, immediate cost to dodge a one-time basis-point move that may already be in the price. And while you sit in cash for a day or two, ordinary noise in the names will swing many times larger than the rebalance, in either direction.

The disciplined move is the unglamorous one: keep holding, and if you have new capital to deploy, let that buy into any post-inclusion softness. The edge is mechanical patience. Don't trade against your own thesis to chase a basis point.

The critics are not cranks

This is not a fringe complaint. The people objecting are the establishment of the indexing world:

- Owen Lamont (Acadian Asset Management) laid out the two core defects — inadequate liquidity requirements and insufficient time for price discovery — in a piece titled, pointedly, "Special treatment for the SpaceX IPO?"

- Jason Zweig (Wall Street Journal) called the changes "arbitrary, unfair and potentially risky."

- Robin Wigglesworth (Financial Times) called the result "the biggest bagholder exercise."

- Nell Minow, the corporate-governance authority, was blunt: "They had to bend the rules to get into the Nasdaq index — they would never qualify normally," and predicted large retirement funds might build alternative indexes that exclude such companies.

- CalPERS and the New York State and City funds — over a trillion dollars between them — objected to being forced into a company they would not choose, over governance concerns including the 82% voting lock.

- Morningstar put SpaceX's fair value at less than half the ~$1.75T IPO target, i.e. the forced buyers are being marched in at roughly double what at least one serious valuation shop thinks the thing is worth.

This is the tell that matters most. The objection is not "SpaceX is a bad company." The objection is that the price is being set by rule-driven forced demand rather than by anyone's judgment of value — which is exactly the claim this series has been making about the top of the index generally. SpaceX is just the case where it is visible to the naked eye, because they had to change the written rules to do it, and someone wrote the changes down.

My lens, owned plainly

I will not hide behind the analysts. Here is what I actually think, in my own voice, before the event:

This is not a scandal that breaks the system. It is the system, finally visible. The reflex is to call Lex SpaceX a corruption of indexing. I think that framing lets everyone off too easy. The forced-buy bid did not appear for SpaceX; it has been the dominant price-setting force at the top of the market for a decade. What is new is only that this time the demand was too big to fit through the existing rules, so the rules were widened and the widening was minuted. We are not watching the machine break. We are watching someone open the casing and point at the gears while it runs.

Index membership has become an engineerable asset, and SpaceX is the template. Get large enough, pick the venue whose committee will move, and design a lockup that manufactures float on a schedule, and you can summon billions in mechanical demand more or less on command. SpaceX made early inclusion a condition of its listing — read that sentence again. The issuer set a term, and the index changed to meet it. Anthropic has filed. OpenAI will not be far behind. The path is now paved, and I expect a procession.

This is why I run SP3, and it cuts both ways. If forced flows set megacap prices, then owning the names that absorb the most forced flow is the rational position — that is the whole strategy. But the same mechanism that supports the top 3 can be turned against any one of them: to fund a manufactured newcomer, every existing constituent gets trimmed, proportionally, including the giants. Concentration at the top is not immune to a new entrant. It pays for the new entrant. SP3 rides the flow; it does not own the flow. That distinction is the risk, and I would rather name it than paper over it.

The next move: bundle to the top

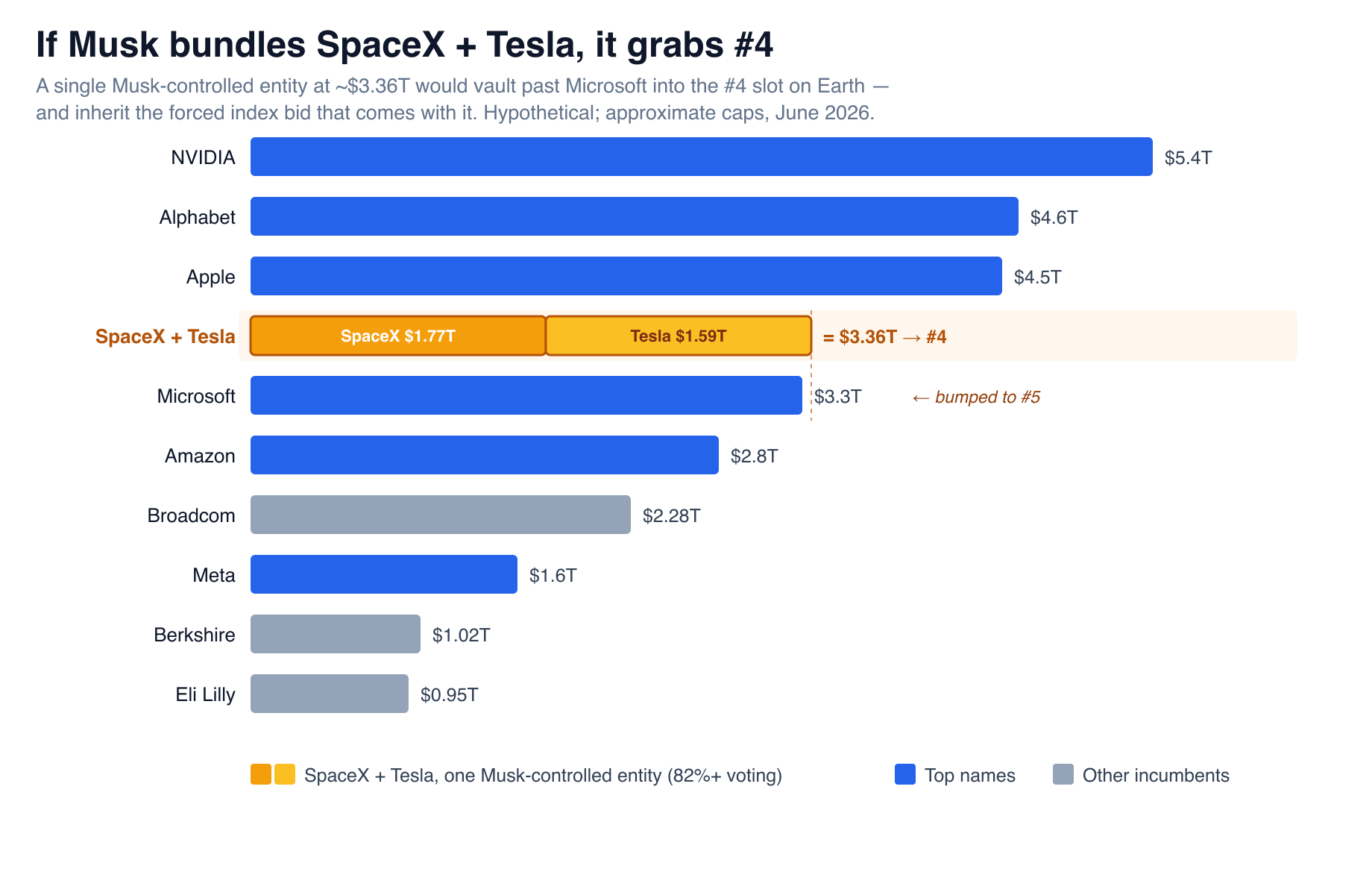

If index membership is an engineerable asset, the SpaceX IPO is only the opening move, and the endgame is visible from here. Musk has all but narrated it — xAI absorbed X in 2025, he has repeatedly mused about combining his ventures, and the rumor that will not die is that SpaceX and Tesla eventually fuse into a single listed entity. Treat what follows as a thought experiment rather than a forecast, and the caps as illustrative. But the arithmetic is unforgiving.

SpaceX comes public at ~$1.77T. Tesla sits at ~$1.59T. Bundle them and you get a single Musk-controlled company at roughly $3.36 trillion — which does not slot in at seventh or eighth. It vaults past Microsoft into the #4 position on Earth, behind only Nvidia, Alphabet, and Apple. One man, with 82%-plus voting control, would sit at number four by index weight, and every passive dollar in America would be required to hold him there — at whatever weight the cap-weighting and the float multipliers dictate.

That is the entire thesis taken to its logical end. The first chart showed SpaceX manufacturing its way onto the edge of the Mag 7 by rewriting the seasoning rules. This is the sequel: you do not have to climb the ranking one company at a time when you can fuse two of them. Float can be manufactured — the tiered lockup. Inclusion can be accelerated — Fast Entry. And size, the thing that determines how much forced flow you command, can be assembled by merger. Each lever is individually defensible; together they convert "the index" from a passive mirror of the economy into a ladder you can engineer your way up.

And notice who pays for the leap. To carry a SpaceX-Tesla bundle at a #4 weight, every index fund trims Microsoft, Amazon, and the rest to fund it — the same reallocation mechanic as a single inclusion, now at four-trillion-dollar scale. The forced bid does not reward the best company. It rewards the best-engineered index position. That is either the most bullish or the most damning sentence I can write about where price formation has gone, and I honestly cannot tell you which.

Predictions I am putting on the record before June 12

Boldness without falsifiability is just noise. So here is my lens, converted into specific calls I am willing to be graded on in the follow-up. I may be wrong on any of these. That is the point of writing them down now.

- The forced bid will be visibly real. In the Nasdaq-100 inclusion window (~early July; the S&P 500 is now deferred a year-plus after S&P's June 4 refusal), there will be a documented, concentrated wave of mechanical buying in the billions, regardless of any news about SpaceX itself.

- Up into inclusion, soft after. Following the Murray–Sammon pattern, SpaceX trades firm or rising into its Nasdaq-100 inclusion and then underperforms the index in the weeks after the forced bid is absorbed. I will define "underperforms" concretely in the follow-up against QQQ from the inclusion date.

- The price will detach from value, and not quietly. The gap between the index-driven price and independent fair-value estimates (Morningstar's "less than half") will be large enough to be the story, not a footnote.

- The giants get trimmed to pay for it. Around each inclusion, the top index names — Apple, Microsoft, Nvidia, Amazon — see measurable mechanical selling pressure to fund the SpaceX weight. The flow is a reallocation, not new money.

- The float multiplier produces a thin, jumpy book. With only 3–5% real float weighted up, post-inclusion volatility runs hot relative to a normal megacap, and the tiered lockup releases are visible as supply events on or near their scheduled dates.

- The template gets reused within twelve months. At least one more megacap private name (Anthropic, OpenAI, or a peer) uses the same fast-entry / engineered-float path. Lex SpaceX becomes Lex Plural.

- Engineered size enters the conversation. Within twelve months, combining entities to climb the index — a SpaceX-Tesla bundle, or a peer's equivalent — goes from rumor to openly discussed strategy by Musk, an index provider, or a major desk. The lever moves from float and timing to size itself.

If most of these hold, the SP3 thesis is not a clever backtest — it is a description of how the market now works, written down before the proof arrived. If they fail, I will say so, in print, with the same specificity.

What is not in dispute

None of the dollar figures above are mine to stand behind as settled — they are sourced third-party estimates that disagree by an order of magnitude, and I have flagged them as such. The predictions above are exactly that: predictions, and I will grade them honestly.

But this part needs no backtest and no forecast, because it is already written into the rulebooks with dates attached: at Nasdaq and FTSE Russell the seasoning, profitability, and free-float requirements were rewritten to admit one company faster, at the company's stated request — and at S&P, under the same pressure, they were defended. Whatever happens to the stock, both of those facts stand. The rest of this essay is my reading of what it means. The follow-up will tell us how good the reading was.

Sources

- SpaceX targets $135 IPO price at valuation of $1.77 trillion — CNBC

- Special treatment for the SpaceX IPO? — Owen Lamont, Acadian Asset Management

- If S&P Dow Jones rewrites its listing rules, SpaceX and Anthropic will benefit — investors won't — Fortune

- "Lex SpaceX"? Nasdaq changes index rules for Musk's IPO — heise online

- SpaceX IPO Index Inclusion: How rule changes for SPY, QQQ, and IWM force funds to sell and buy SpaceX — SpotGamma

- The SpaceX IPO has an unusual lockup policy for insiders — Motley Fool

- SpaceX insiders will get to sell shares earlier than usual after the IPO — CNBC

- SpaceX is coming to your retirement account. Not everyone is thrilled. — NBC News

- S&P mulls new index rules to speed up addition of mega IPOs — Bloomberg

- New rule could fast-track SpaceX IPO for Nasdaq index inclusion — Yahoo Finance

- Morningstar: SpaceX worth less than half its $1.75T IPO target — CNBC

- Academic: Murray & Sammon (2026) on seasoning periods; Jiang, Vayanos & Zheng (2022) on passive demand and the largest 50 firms; VinFast (Aug 2023) low-float precedent.

- S&P Dow Jones decision (June 4, 2026), declining the megacap fast-entry rules for the S&P 500: Bloomberg; CNBC; Axios.

- NVIDIA Q1 FY2027 (reported May 2026): +$80B buyback authorization + 2,400% dividend increase — Motley Fool; record Q1 payouts and the $80B buyback — Yahoo Finance; revenue $81.6B (+85% YoY), ~$20B returned in the quarter, dividend $0.01→$0.25/share payable June 26, 2026.

- Napkin-math inputs: S&P DJI — ~$20T benchmarked / ~$13T indexed to the S&P 500 (per S&P DJI; figure as of the Feb 2026 update); S&P 500 total market cap ~$63–68T in 2026 — GlobalData; US ETFs: record $1.5T net inflows in 2025; VOO +$137.7B — etf.com; Apple $100B buyback authorization, 2025; NVIDIA +$60B buyback (Aug 2025), ~$52B repurchased over the 12 months through Sep 2025.

Written before the bell, ahead of the June 12 IPO. A follow-up will grade the predictions above against what actually happens. The dollar figures throughout are sourced third-party estimates that disagree by an order of magnitude; the predictions are mine, and falsifiable.

Related Posts

When the King Falls: Backtesting the Sovereign Exit Rule

I built the SP3 thesis on the idea of never selling. The backtest says tight rotation beats never-sell by 17% in terminal wealth — and both crush SPY.

The Top Three And The Tundra

The rigged game of passive-flow concentration, the quantitative proof that it's rigged, and how I've decided to play anyway — with a 2006 pickup truck...

The Rent Collector's New CEO: What Apple's Ternus Pick Really Means

Apple picked a hardware engineer to succeed Tim Cook. It is a steelman pick — and a tell about the bench, the privacy trap, and the next decade of App...

Subscribe to the Newsletter

Get notified when I publish new blog posts about game development, AI, entrepreneurship, and technology. No spam, unsubscribe anytime.

Comments

Loading comments...

Published: June 5, 2026 4:14 AM

Last updated: June 5, 2026 4:14 AM

Post ID: da2fe3b2-6b64-4f01-9d48-8c139be03315